![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Core point of view:

Demand resilience is strong, supply and supply are accelerated, and supply and demand gaps are widening. Due to the expansion of the supply side reform, the fourth batch of central environmental supervision, high temperature, floods, etc., the industrial production data fell in July, but the land purchases rebounded, the credit unions exceeded expectations, and the PMI export orders were good. Type and demand resilience are strong. At the same time, in the case of a basically stable demand side, the market has been clear since 2012, superimposed supply-side reforms and environmental protection pressures since 2016, and the fourth batch of central environmental supervision and supply-side reforms in the second quarter of 2017. The expansion of the supply and demand gap, which is the root cause of the surge in the price of periodic products, the continuous improvement of corporate profits, and the recovery of balance sheet time exceeded expectations.

With the advent of the peak season in autumn, demand is expected to improve, coupled with environmental protection, supply and other constraints to increase production capacity, we maintain economic long, supply a fresh cycle judgment.

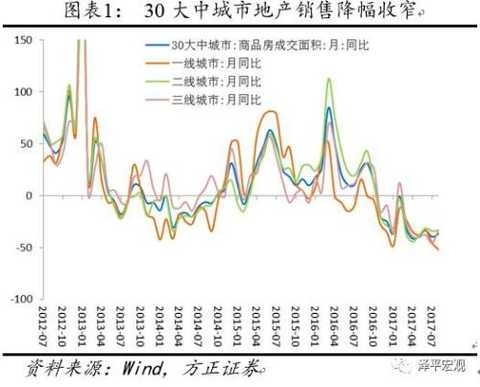

The decline in downstream real estate sales has narrowed, and land supply in first-tier cities has increased significantly. The sales of 30-city real estate sales narrowed year-on-year, with a year-on-year increase of -36.7% in August, an increase of 3.1 percentage points from July; the land turnover of the top 100 cities in early August was -7.59%, down from 0.9% in July. At the beginning of August, the national land supply increased sharply year-on-year. Especially in the first-tier cities, the land supply increased from -0.1% in July to 80.3%. In August, the auto market started stronger, and the retail sales in August increased by about 5.8% year-on-year. The demand for textile clothing weakened; the container freight index slowed down year-on-year, and the freight price and BDI index increased.

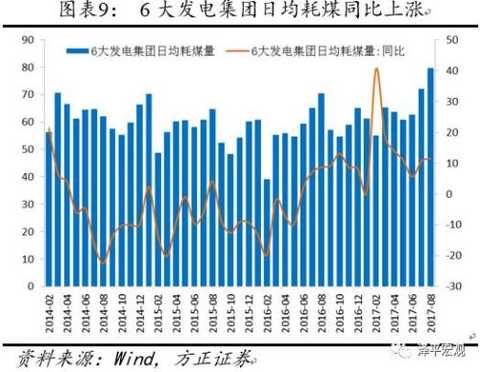

Coal consumption in the middle reaches of power generation accelerated year-on-year, steel prices fell slightly, cement stabilized machinery sales were hot, commodity prices rose sharply, and the price of aluminum was greatly increased. In August, the average daily coal consumption of the 6 largest power generation groups increased by 11.5% year-on-year, higher than the 10.6% in July. Domestic blast furnace operating rate rebounded last week. In July, the average daily output of crude steel reached 2.388 million tons, down 2.2% from the previous month. August rebar prices rose 59.9% year-on-year, up from 58.3% in July. Supply compression, the peak season is coming, steel is expected to heat up in the future. Cement prices fell by 0.1% this week. Cement prices in August increased by 27.1% year-on-year, down from 31.7% in July. Last week, the national cement storage capacity reached 66.6%, lower than the previous value of 68.0%. The chemical product market is generally stable. Sales of construction machinery in July was hot. From January to July this year, the cumulative sales of 25 excavators in 25 mainframe manufacturing enterprises increased by 111.7% year-on-year. Heavy truck sales continued to grow at a high level. In July, domestic heavy truck sales increased by 81.4% year-on-year, with sales of 90,200 units, which changed the past year's off-season. The probability of a US rate hike has further declined, and the Trump Dissolution Business Advisory Board has caused the dollar to continue to weaken. The increase in US oil production has caused market oversold concerns, EIA stocks are less likely to be recognized by the market, and crude oil prices have fallen sharply. The implementation of the reform and implementation led to a sharp rise in aluminum prices.

The price of vegetables fell back to the bottom of the pig price, the price of medicines slowed down year-on-year, and the short-term interest rate rose slightly. The price of fresh vegetables began to fall in August, and the price of pork decreased year-on-year. The price of Chinese herbal medicines slowed down year-on-year. In addition to Tuesday, the central bank conducted reverse repurchase operations on Monday, Wednesday and Thursday, with reverse repurchase amounts of 210 billion, 280 billion and 100 billion. On Monday, the reverse repo fully hedged the amount due on the day, with a net investment of 180 billion on Wednesday and a net investment of 50 billion on Thursday. The central bank will continue to maintain a stable and neutral monetary policy, maintaining a smooth and moderately neutral liquidity. This week's R007 interest rate was 3.9933%, up 87.04 BP from last week; DR007 interest rate was 2.9132%, up 7.59 BP from last week; 1-year government bond yield was 3.3350%, down 0.63 BP from last week; 10 years Treasury yields were 3.5988%, down 1.75 BP from last week. The US dollar index rebounded and the RMB exchange rate fell.

Risk warning: Fed rate hike exceeded expectations; domestic currency tightening and financial deleverage exceeded expectations; real estate regulation is too tight; reform is lower than expected; debt risk.

text:

1. Downstream : The decline in real estate sales has narrowed, and the supply of land has increased.

This week, 30 large and medium-sized cities real estate sales fell by 6.8%. As of August 14, real estate sales in 30 large and medium-sized cities were -36.70% year-on-year, up from -39.8% in July; among them, first- and third-tier cities were -52.04%, -33.31% and -33.04%, respectively, below Above and above July, -45.5%, -34.3% and -46.0%. The land transaction area in early August fell year-on-year. In August, the turnover of land in large and medium-sized cities was -7.59% year-on-year, down from 0.9% in July, with the first-line increase from 41.2% in July to 50.87%; the second-line fell to -30.68% from 7.7% in July; The third line increased from 1.6% in July to 21.73%. The year-on-year decline in land transaction area was mainly due to the decline in land acquisition in second-tier cities. At the beginning of August, the land supply of 100 large and medium-sized cities increased by 34.64% year-on-year, which was significantly higher than that of July--11.7%. The year-on-year growth rates of land supply in first- and third-tier cities were 80.30%, 37.51% and 28.41% respectively, which was higher than that in July. -0.1%, -15.4% and 22.6%.

The car market started in August. In terms of retail sales, the year-on-year growth rate in August this year was about 5.8%, and the growth rate in the first two weeks was 49% and 14% respectively. In addition, according to the latest data released by the National Federation of Passengers Association this week, the total output of narrow-seat passenger cars decreased by 4.6% in July and 2% year-on-year. The overall situation of the automobile market was good.

Last week, the box office receipts of the movie dropped by 29.2%, and the number of movie attendances and screenings were -28.1% and 0.9%, respectively. The main reason was that the "Wolf 2" heat began to fade, and the newly released films were weak at the box office. On a year-on-year basis, the box office receipts and movie attendances in August were 149.2% and 129.1%, respectively, significantly higher than the 6.4% and 2.6% in July. The main reason was the phenomenal film "Wolf 2", which was constantly refreshed since the release. Domestic movie box office record. The number of screenings in August was 21.7% year-on-year, basically the same as in July.

The year-on-year growth rate of textile raw materials continued to slow down. The yarn price index in China's textile economic information index rose by 0.09% from the previous month to 3.9% in August, down from 8.4% in July. The grey cloth price index fell by 0.01% from the previous month to 1.1% in August, down from 3.6% in July. In the Keqiao Textile Price Index, raw materials, grey cloths, apparel fabrics and home textiles decreased by 0.13% year-on-year, up by 1.61%, up by 0.31%, up by 0.44%, respectively, higher than last week's -0.23%, -1.22%, -0.11 % and -0.11%.

On August 15th, GfK released the “China Digital Home Appliances Trend Report for the First Half of 2017â€, showing that the online share of China's home appliance and consumer electronics market will reach 29% in 2017. Tmall has become the leading structure of home appliances. The first platform to upgrade.

The container freight index slowed down year on year, and the freight price and BDI index increased. Last week, the Shanghai Export Container Freight Index (SCFI) fell by 2.1% from the previous month, compared with 41.5% in August, up from 26.4% in July. China's export container freight index (CCFI) fell by 1% quarter-on-quarter, compared with 22.1% in August, down from 28.2% in July. Domestic and international freight prices have increased from the previous month. This week, the Baltic Dry Index (BDI) rose by 2.7% from the previous month to 58.1% in August, up from 28.1% in July. Last week, China's coastal dry bulk freight index (CCBFI) rose by 0.6% month-on-month, compared with 11.4% in August, down from 19.9% ​​in July.

2. In the middle reaches: the growth rate of coal consumption for power generation is rising, and the price of steel is slightly lower.

Power generation coal consumption increased this year. The average daily coal consumption of the 6 major power generation groups increased by 2.7% from the previous month, which was 3.5 percentage points higher than the previous value. As of August 17, the average daily coal consumption of the six major power generations was 796,000 tons, up from 782,000 tons last week and 721,000 tons in July. The coal consumption of power generation in August increased by 11.5% year-on-year, higher than the 10.6% year-on-year in July. Since August, the temperature has decreased in all parts of the country. The decline in domestic electricity consumption has highlighted the growth of industrial electricity consumption. The prices of some bulk commodities such as steel, coal and nonferrous metals have been strong, driving the production of steel, petroleum processing, coking and other energy and raw materials industries. Conducive to calming prices up too fast, the application of electricity has also increased.

The profit ratio of domestic steel mills has been flat at 85.89% for the fourth consecutive week, the highest since April 2017. Last week, the national blast furnace operating rate was 77.5%, higher than the previous value of 0.4 percentage points. The increase in blast furnace start-up was mainly due to the increase in the start of the blast furnace of small and medium-sized steel enterprises and the resumption of production of the blast furnace in the previous period. According to the National Bureau of Statistics, the national crude steel output in July was 74.02 million tons, and the average daily output was 2.388 million tons, down 2.2% from the previous month and up 6.7% year-on-year, up from 3.4% in June. As steel demand enters the peak season and supply is compressed, the market is expected to heat up. Rebar prices fell slightly this week, with the average price falling by 0.6%. August rebar prices rose 59.9% year-on-year, up from 58.3% in July.

The national cement price is stable, and the market outlook is expected to pick up. Cement prices fell 0.1% month-on-week this week, up 27.1% year-on-year in August, down from 31.7% in July. Last week, the national cement storage capacity reached 66.6%, lower than the previous value of 68.0%. In the first half of the year, measures such as peak production and environmental protection have improved market supply and demand. In 2017, the absolute value of cement storage capacity was significantly lower than that of the same period last year. As the cement season comes to an end, the future price will rise as supply and demand improve.

The chemical products market continued to maintain its upward trend. There were 33 products in the chemical sector that rose by a quarter-on-quarter. The top three commodities were TDI (43.9% MoM, up 153.3% YoY, up 66.2% from last week) and propylene oxide (27.3% MoM). It increased by 37.1% year-on-year, up 28.0% from last week. Butadiene increased by 10.5% from the previous month and increased by 7.5% year-on-year, up 10.9 percentage points from last week. There were 29 kinds of products with a decrease in the chain, and the top 3 products were maleic anhydride (99.5%) (down 5.0% from the previous month, up 38.9% from the previous year, down 6.8 percentage points from last week) and hydrofluoric acid (down 3.3% from the previous month). It increased by 27.0% year-on-year, down 4.4 percentage points from last week, and fatty alcohol (down 3.1% from the previous month, up 10.1% year-on-year, down 6.2 percentage point from last week).

Construction machinery sales in July rose sharply year-on-year. According to the statistics of the Mining Machinery Branch of China Construction Machinery Industry Association, 25 mainframe manufacturing enterprises that were included in the statistics from January to July this year sold a total of 82,725 types of excavation machinery products, a year-on-year increase of 101.3%. The domestic market sales (excluding Hong Kong, Macao and Taiwan) were 77,814 units, a year-on-year increase of 111.7%. The export sales volume was 4884 units, a year-on-year increase of 14.0%. In July, a total of 7565 excavation machinery products were sold, up 108.9% year-on-year. The domestic market sold 6,993 units, up 126.0% year-on-year. Export sales reached 659 units, up 15.4% year-on-year. Heavy truck sales continued to grow at a high level in July. According to the statistics of the China Automobile Association, the domestic heavy trucks increased by 81.4% in July, with a total sales volume of 90,200 units, which changed the cold weather in the off-season in previous years. In 2017, heavy trucks have maintained rapid growth for 7 consecutive months. From January to July, the cumulative sales of heavy trucks in China increased by 637,900 units, a year-on-year increase of 72.28%.

3, upstream: oil prices are still low, strong color

This week, the CRB industrial raw materials index fell by 0.17% from the previous month to 11.4% in August, up from 10.3% in July. SOUTH index industrial chain increased 2.33%, an 38.1% in August, 34.2% higher than an Jul; South China Agricultural 000061, diagnosis stock index decreased 0.21%, up 2.1% in August, up 0.2% higher than in July.

The probability of raising interest rates continues to decline, and the US dollar index continues to weaken. The US dollar index remained stable this week, with -2.1% in August, down from -1.6% in July. The minutes of the Fed's July meeting showed that weak inflation seems to make policymakers more cautious, interest rate hikes may be delayed during the year, Trump disbanded two business advisory committees, and the dollar fell again after a small gains stabilized. Stimulated by the US dollar, gold rose slightly, but the weakening of demand could not support the continued sharp rise of gold. This week, London spot gold increased by 0.1% from the previous month, and August was 0.0%, up from 7.6% in July.

The US inventory report was not effective, and oil prices fell under pressure. This week, WTI crude oil prices fell by -5.6% from the previous month, and rose 9.2% year-on-year in August, up from 4.2% in July. The sharp drop in US crude oil inventories failed to dispel investors' oversupply concerns. The weak demand from the US and China's two major crude oil consumer countries showed a sharp rise in the downside risk of oil prices. In the week of August 11th, EIA crude oil inventories - 8.945 million barrels, the lowest level in a single week since October 2015, expected -338.20 million barrels; gasoline inventory + 22,000 barrels, expected -90 million barrels.

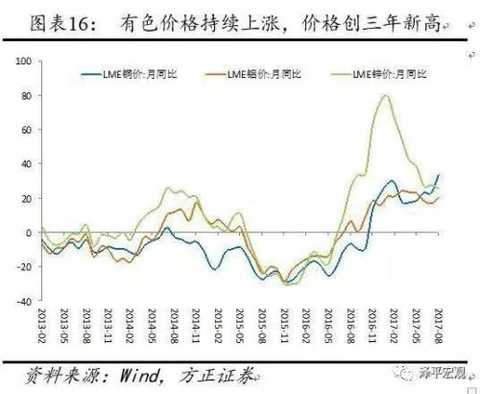

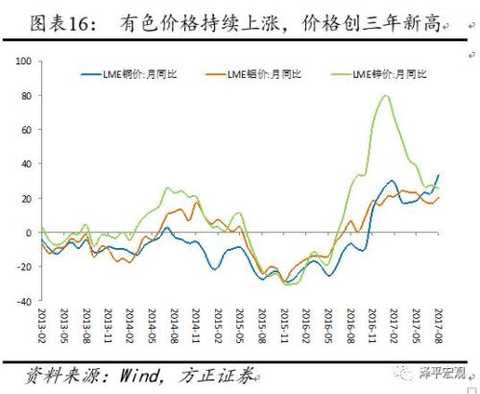

Non-ferrous prices continued to rise, and copper, aluminum and zinc prices all hit new highs in the past two years. The environmental protection efforts continue to increase, and the supply contraction drives the non-ferrous metals to continue to rise. LME copper increased by 0.45% this week, compared with 33.7% in August, up from 23.1% in July. LME aluminum prices increased by 0.76% on a week-on-week basis, compared with 20.4% in August, up from 16.8% in July. LME zinc prices increased by 1.80% on a week-on-week basis, compared with 25.7% in August, down from 27.5% in July.

4. Price: The price of vegetables will fall back to the bottom of the pig price, and the price of oil and medicine will continue to fall.

The average wholesale price of 28 key vegetables monitored by the Ministry of Agriculture decreased by 1.0% this week. The Qianhai Vegetable Wholesale Price Index increased by 1.8% from the previous month. The influence of high temperature weather in Shandong on supply was weakened, and the vegetable wholesale price index decreased by 6.1%. The average wholesale price of 28 key vegetables for monitoring in the Ministry of Agriculture, the wholesale price index of Qianhai vegetables and the wholesale price index of vegetables in Shandong were 4.9%, 1.1% and 20.7% respectively in August, which were higher than the 2.8% in July and lower than respectively. 2.7% and above 20.1%.

The average wholesale price of pork in the Ministry of Agriculture increased by 0.9% from the previous month, and fell by 20.2% in August, up from -22.8% in July. The average retail price of pork in 36 cities rose by 0.2% month-on-month, compared with -10.0% in August, which was higher than the -11.3% in July and -11.5% in June. The National Development and Reform Commission warned that pork supply may increase further in the second half of the year, and the overall pig price will continue to decline. The average retail price of beef and mutton in 36 cities was -0.3% and -2.5% in August, respectively, higher than -1.0% and -2.8% in July. The average retail price of grass carp and carp in 36 cities was 9.7% and 3.7% respectively in August, down from 10.6% and 5.4% in July.

In the non-food sector, drug prices fell year-on-year. China's Chengdu Chinese herbal medicines price index was 8.4% in August, down 1.9 percentage points from July's 10.3%.

5. Currency: Monetary policy is “tight balanceâ€, short-term interest rates rise across the board

This week, the central bank's open market has a total of 600 billion reverse repurchase maturity, which expires 210 billion, 140 billion, 100 billion, 50 billion and 100 billion respectively from Monday to Friday. In addition, there are 287.5 billion MLF and 80 billion treasury cash deposits due on Tuesday and Friday, respectively.

Last Friday, the central bank carried out a 70 billion 7-day, 60 billion 14-day reverse repurchase operation, fully hedging the amount due on the day. On Monday, the central bank opened the market for 110 billion 7 days, 100 billion 14 days reverse repurchase operations, fully hedging the amount of the day. On Tuesday, the central bank conducted an MLF operation of 399.5 billion yuan, with a variety of one-year period, and the interest rate was steady at 3.20%, with no repurchase operations. On Wednesday, the central bank's open market will carry out 150 billion 7 days, 130 billion 14 days reverse repurchase operations, with a net investment of 180 billion. On Thursday, the central bank opened up the market for 60 billion 7 days, 40 billion 14 days of reverse repurchase operations, with a net investment of 50 billion.

In August, the central bank’s capital maturity was large, but in light of the recent central bank’s open market operations, the central bank still maintained the “maintenance of liquidity and moderate neutrality†proposed in the previous quarter’s monetary policy report, and a stable neutral monetary policy. No change has taken place.

As of August 18, the 1-day inter-bank repurchase plus rights ratio was 3.0802%, up 25.93 BP from last week; the 7-day inter-bank repurchase plus rights ratio was 3.9393%, up 87.04 BP from last week. The 1-day deposit-type institution’s repurchase rate was 2.8627%, up 9.95 BP from last week; the 7-day deposit-type institution’s repurchase rate was 2.912%, up 7.59 BP from last week. The one-year government bond yield was 3.3350%, down 0.63 BP from last week; the 10-year government bond yield was 3.5988%, down 1.75 BP from last week.

The direct interest rate (monthly interest rate) of the Pearl River Delta Bill, the direct interest rate of the Yangtze River Delta Notes (monthly interest rate) and the interest rate of the bill transfer (monthly interest rate) were all the same as last week. This week's credit differential differentiation for different periods, the credit spread of 1-year AAA corporate bonds decreased by 3.15 BP, and the credit spread of 10-year AAA corporate bonds expanded by 1.33 BP.

The US dollar index rebounded and the RMB exchange rate fell. This week, the US dollar appreciated by 0.21% against the central parity of the yuan, the US dollar against the RMB spot exchange rate rose by 0.43%, and the offshore RMB depreciated by 0.33%. The onshore and offshore RMB exchange rate spreads narrowed from -0.0077 last week to -0.0191. The US dollar against the RMB 1-year foreign exchange forward purchase price fell by 9 BP, the long-term depreciation pressure decreased.

Artificial Leather,Stretch Leather Fabric,Tpu Synthetic Leather,Pu Synthetic Leather For Shoes

WENZHOU JOVAN INTERNATIONAL COMMERCIAL , https://www.wzjovan.com